What is GSTR 9?

- It is the Annual Return

- It is required to be filed after the end of the Financial Year

- It will be filed only once in a year

- It contains the details of supplies made and received during the year under different tax heads i.e. CGST, SGST and IGST. It consolidates the information furnished in the monthly or quarterly returns during the year.

Who is required to file GSTR 9?

All the registered taxable persons under GST must file GSTR 9. However, the following persons are not required to file GSTR 9

- Taxpayers opting Composition scheme as they must file GSTR-9A

- Casual Taxable Person

- Input service distributors

- Non-resident taxable persons

- Persons paying TDS under section 51 of GST Act.

Types of Annual Returns

Nil Annual Return: As long as the person is registered under GST, even in case of Nil GST liability for the year, he will be required to file return.

Note: However 31st GST Council meeting held on 22nd December 2018 recommended further extension for filing GSTR-9,GSTR-9A and GSTR-9C upto 30th June 2019.

Details of GSTR 9:

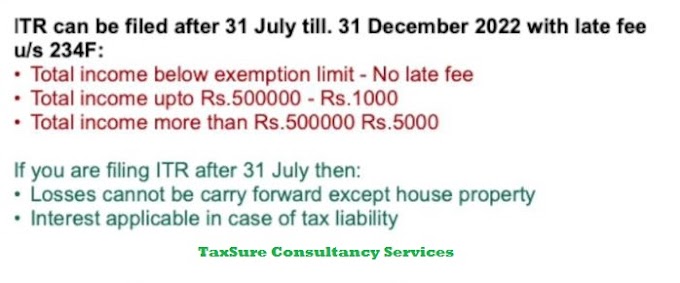

Penalty for Late filing of GSTR 9: Late fees for not filing the GSTR 9 within the due date is Rs. 100 per day per act, up to a maximum of an amount calculated at a 0.25% of the turnover in the state or union territory. Thus there is no late fee on IGST.

Important Points to be noted:

- It is clarified that ITC cannot be claimed in GSTR-9- Annual return. So any Liability identified later during the filing of GSTR 9 is to be deposited with the government in Form DRC-03. (It means it should be paid in cash rather than by claiming ITC to that extent).

- Reconciliation of the books of accounts and tax invoices are issued during July 2017 to Mar 2018 is of utmost importance; this should match the turnover declared in the audited financial statements. It is important for the figures in the books of accounts and the invoices to match or else the GST paid will be incorrect. Along with the invoices, debit and credit notes shall also be in agreement with books of accounts.

- The Tax Invoices issued during the period and the E Way Bill Data should be matched.

- Purchase Invoices should be agreed with Books and it must be ensured that the respective sales data of the respective suppliers is also uploaded in GSTR 1 so that such data will be appeared in GSTR 2A of the purchaser. Otherwise there will be mismatch in the ITC claimed and ITC paid on purchases.

0 Comments